The pros and cons of dividend reinvestment plans

Disclaimer: The below article is for informational purposes only and does not constitute a specific product recommendation, or taxation or financial advice and should not be relied upon as such. While we use reasonable endeavours to keep the information up-to-date, we make no representation that any information is accurate or up-to-date. If you choose to make use of the content in this article, you do so at your own risk. To the extent permitted by law, we do not assume any responsibility or liability arising from or connected with your use or reliance on the content on our site. Please check with your adviser or accountant to obtain the correct advice for your situation.

If you invest in a dividend-paying stock, you may be given the option to establish a dividend reinvestment plan (also known as a DRIP or DRP). While automatically reinvesting dividends can be a convenient way to grow your portfolio, there are several factors to keep in mind before deciding to partake in a DRP.

This article will cover:

- What is a dividend reinvestment plan?

- How DRPs work

- Automatically reinvesting dividends

- Pros of dividend reinvestment plans

- Cons of dividend reinvestment plans

- Taxes and dividend reinvestment plans

What is a dividend reinvestment plan or DRIP?

Dividend reinvestment plans or DRIPs (DRPs in Australia and New Zealand) allow investors to reinvest their cash dividends to purchase new shares in a company. DRPs allow for direct acquisition of shares from the company itself, sometimes at a discount to the market value, and involve no brokerage fees.

How does a dividend reinvestment plan or DRIP work?

Before jumping into the advantages and disadvantages of dividend reinvestment plans, here’s an example of how they work:

Let’s say you own 1,000 shares in company X. You have chosen to participate in its DRP so that 100% of your dividends are reinvested.

The company announces a dividend of 15 cents per share and the shares have a market value of $10.50 each.

You would normally receive $150 in the form of a cash dividend (1,000 x $0.15). However, because you’re enrolled in the DRP, you receive 14 shares (14 x $10.50 = $147), which increases your total holding to 1,014 shares. Because the remaining $3 isn’t enough to buy a share, the amount is carried forward to the next dividend payment.

Can you automatically reinvest dividends?

If a company you are invested in offers a dividend reinvestment plan, your dividends will be automatically reinvested to acquire more of the company’s shares. This can be set up through the company’s share registry or fund issuer, or in some cases, through your broker.

Pros of dividend reinvestment plans

Taking the above into consideration, there are a number of advantages that DRPs offer investors, including:

No brokerage fees

Reinvested dividends enable the acquisition of new shares/stocks with no brokerage fees. This makes for a very cost-effective method for buying new shares over time. Not having to pay brokerage fees can make a big difference, especially for small trades, as they are one of the main expenses for investors which eat into returns.

Dollar cost averaging

Dollar cost averaging is a strategy where investors buy the same amount of shares on a regular interval, building savings and wealth over a long period. DRPs incorporate a similar idea, with your money being regularly reinvested back into the same company, and gradually growing your holdings. At times, the shares will be purchased when they are overvalued, and at other times when they are undervalued. However it should even-out over time. As a result, investors will have less tendency to make an emotional buy/sell decision, as they have a set strategy in place.

Purchase discount

Sometimes DRPs offer new shares with a discount to the market price. These discounts can range from 1 - 5% and can be a great incentive to partake in a DRP.

Capital management tool for companies

DRPs also benefit companies, as they utilise the scheme to retain capital, paying dividends in the form of newly issued shares. As a result, the company maintains its capital, which can then be reinvested back into the business for future growth.

Simplifies the investment process

DRPs appeal to “set-and-forget investors”, as they can simplify their investing strategy by automatically reinvesting their dividends in new shares. This makes it very easy to grow their portfolio without needing to spend much time or attention on their investments.

Saving strategy

DRPs can be considered a form of forced or passive saving as you don't ever personally receive any of the dividend money, therefore cannot be tempted to spend it.

Compounding growth

Grows your portfolio value incrementally, providing the benefit of compounding as each time a DRPs is offered, you will receive a larger number of shares than the previous time (if dividend payouts are unchanged).

No lower limit

There is no lower limit on the number of shares that are required to be owned by an investor, meaning all investors are eligible and able to benefit from dividend reinvestment plans.

Cons of dividend reinvestment plans

Now that we’ve covered the positive aspects of DRPs, let’s look at the reasons many investors avoid DRPs.

No control over price or time

Investors who partake in a DRP do not have any control over the time and price that the shares are purchased, as they are automatically “purchased” on the dividend payout date. This means that you could be buying when the shares are very expensive (although the reverse could be true too – see “dollar cost averaging”, above). Over a long period, this effect usually balances out, being no better or worse off. For less sophisticated investors who don’t continually monitor and try to predict share prices, this will make little difference. However, for more advanced investors, this is considered a significant drawback.

Unbalanced portfolio allocation

Registering for an automatic DRP can be an attractive way to grow your investments. However, this can lead to your portfolio being heavily weighted in certain areas, and unbalancing your target portfolio allocation. Therefore, it is essential to monitor your portfolio allocations, rebalancing them as necessary.

Reduces diversification

For many investors, dividend income is used to initiate new positions in different shares. However, in DRPs, dividend payouts are directly reinvested back into the same company, potentially preventing the establishment of new holdings and thus leading to a lack of portfolio diversification over time.

Not suitable for short-term investors

DRPs are not suitable for short term investors as purchasing the shares on the market is much faster compared to obtaining shares through a DRP. This is especially true for stocks that pay dividends quarterly or bi-annually, rather than monthly. Therefore, it is often much better for shorter-term investors to take the cash dividend and purchase shares separately.

No income stream

As DRPs require sacrificing cash in exchange for new shares in the company, it removes the stream of income that is associated with dividend payments. For a retiree or someone who depends on dividends to support their living expenses, this strategy is not ideal.

Dilution of ownership

DRPs dilute the ownership for an investor in a company as new shares are issued, meaning to maintain the same level ownership, more shares need to be purchased. A maximum level of participation may be introduced to reduce this dilutive effect, discouraging institutional shareholders from participating.

Tedious record keeping

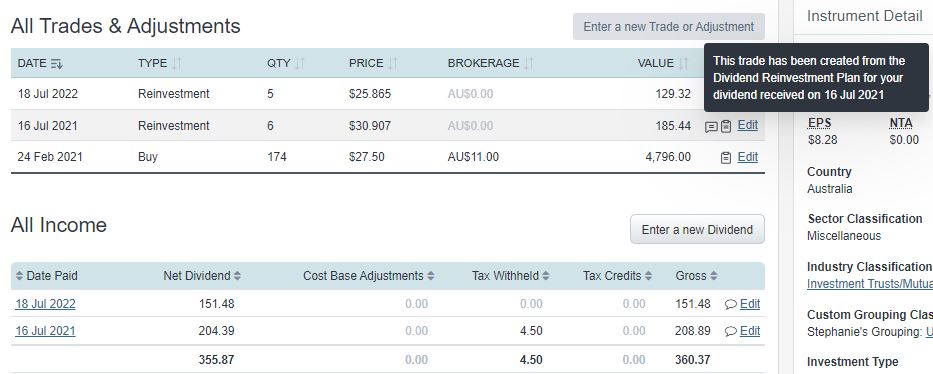

DRPs require both the share purchase price and dividend payment amount to be recorded each time for every dividend payment. This can be very painful to keep track of, especially with a large portfolio. However this portfolio admin problem can be easily solved by using a dedicated portfolio tracker such as Sharesight. For more info, see: How to track a dividend reinvestment plan.

It’s easy to keep track of your DRPs/DRIPs with Sharesight’s Auto Dividend Reinvestment feature.

It’s easy to keep track of your DRPs/DRIPs with Sharesight’s Auto Dividend Reinvestment feature.

Is DRIP investing worth it?

The decision to reinvest dividends or not is ultimately up to the investor. As mentioned above, on the one hand, DRPs can be a convenient and cost-effective way to increase the value of your portfolio and take advantage of compounding growth over time. On the other hand however, participating in a DRP means that you forgo the opportunity to use your dividends as income and unless you are using an automatic portfolio tracker like Sharesight, you will be subjected to tedious manual record-keeping to keep track of your reinvested dividends.

Tax on reinvested dividends

Australia

As per the ATO, for capital gain purposes, DRPs are treated as if you had received the dividend and then used it to purchase additional shares. Franking credits are dealt with in exactly the same manner. If you received a discount, it is not considered taxable income at the time of purchase, rather it is included in the CGT at the time of sale.

When selling shares that have been issued through a DRP, the cost base for the CGT is determined by the market price of the shares at the time of purchase. This is the true price paid for the shares, including any discounts to the share price, which your CGT will be based on.

Canada

If a Canadian investor chooses to take part in a DRIP, their ordinary taxable dividend is subject to the gross-up (for Canadian companies) and dividend tax credit provisions that are faced by all dividends. The new shares that have been acquired through a stock dividend are deemed to have been acquired at a cost equal to the stock dividend amount. When selling their investment, the CGT is applied where the difference between the adjusted cost base (ACB) and the net proceeds received is considered a capital gain or loss. Investors partaking in a DRIP within a tax-free RSP or TFSA account don’t have to worry about this, but those investing in taxable accounts may want to read this article on the tax treatment of Canadian dividend paying stocks.

U.S.

As per the IRS, if you choose to reinvest your dividends in a DRIP, the IRS treats this as two different events. First, the dividend is treated as taxable income, with no difference from a regular dividend payout. Second is the share purchase and future sale where the capital gains will be later taxed.

Some U.S. companies also allow for investors to purchase additional shares of a stock at below market price, in this case, the cash reinvested, and the fair market value of the stock are taxed as ordinary dividend income.

Track the impact of dividends on your investment performance

With Sharesight’s advanced dividend tracking and performance reporting features, investors can access unparalleled insights into their investments at the click of a button. With Sharesight investors can:

- Automatically track your dividend and distribution income from stocks, ETFs, LICs and Mutual/Managed Funds – including the value of franking credits

- Use the Dividend Reinvestment Plan (DRPs/DRIPs) feature to track the impact of DRP transactions on your performance (and tax)

- Run powerful reports to calculate your dividend income with the Taxable Income Report, portfolio diversity and Capital Gains Tax obligations (Australia and Canada)

- Easily share access of your portfolio with family members, your accountant or other financial professionals so they can see the same picture of your investments as you do

Sign up for a free Sharesight account and start tracking the impact of dividends on your investment portfolio today!

![]()

FURTHER READING

You can time the market – and ETFs are the way to do it

Marcus Today founder and director Marcus Padley discusses timing the market, and how investors can do this using exchange-traded funds (ETFs).

Morningstar analyses Australian investors’ top trades: Q1 2025

Morningstar reviews the top 20 trades by Australian Sharesight users in Q1 2025, and reveals where their analysts see potential opportunities.

Sharesight product updates – April 2025

This month's focus was on improving cash account syncing, revamping the future income report and enabling Apple login functionality.