What are the new Employee Share Option Plan disclosure exemptions?

An Employee Share Option Plan (ESOP) is a scheme that companies can use to offer their eligible workers the option to purchase company shares at a specific price in the future. From 1 October 2022, new rules are in place, making it easier for startups to manage their ESOPs.

Previously, if a startup wanted to offer shares to more than 20 employees in a year (excluding senior managers), they had to comply with complicated disclosure rules. However, under the new changes to the Corporations Act 2001, startups no longer have to follow existing disclosure obligations if they structure their ESOP offers according to the new employee share scheme rules. This article explains these new ESOP disclosure exemptions and how your company can comply with the new regulations.

What are the requirements for your ESOP offer?

If your ESOP requires participants to pay to acquire their shares or options, the terms of your ESOP and the offers made under it must meet specific requirements.

1. ESOP Terms

First, ESOP participants must fall within specific classes of persons. For example, eligible participants include:

-

Directors;

-

Employees; or

-

Other service providers.

Second, the securities issued under your ESOP must be ESS interests, per the Corporations Act. Accordingly, ESS interests include fully paid shares and options to acquire fully paid shares.

2. Terms of the offer under the ESOP

The terms of the offer made under the ESOP must comply with an issue cap and a monetary cap.

The issue cap refers to the maximum number of shares your company can issue under the ESOP. To comply with the issue cap, you must reasonably believe, at the time of making the relevant offer, that:

-

You can issue the total number of fully paid shares under that offer; and

-

The total number of shares you have, or could have, issued under your ESOP in the previous three years is no greater than 20% of the company’s total issued shares.

Keep track of the offers made under your ESOP to stay within the cap. Nevertheless, you can increase the issue cap above 20% if your company’s constitution allows it.

Additionally, the monetary cap refers to the total amount a participant can pay under your ESOP. The amount participants pay (or is payable) for their shares or options cannot exceed AU$30,000 in the 12 months following the participant accepting their offer, plus:

-

70% of the dividend value the participant or a related person received in connection with the ESOP in those 12 months; and

-

70% of any cash bonuses the participant received in those 12 months.

The monetary cap can accrue over five years up to a maximum accrual of $150,000.

What information do you need to provide?

If your ESOP and the relevant offers meet the above requirements, you must provide certain simplified disclosure materials to participants under your ESOP at specific times.

| Documents | Description |

| Offer statement | You must include a statement that you are making the offer under Division 1A of Part 7.12 of the Corporations Act. |

| ESOP offer document | The documents you must provide participants when they receive their offer must include the following:

|

| Supporting information statement | Suppose your ESOP is an option plan. If so, the offer letter you issue to participants must include a statement that they cannot exercise options unless you provide the "simplified disclosure materials" at least 14 days before the exercise of the option or the vesting of the right to exercise. |

You must provide this information to the relevant participant 14 days before they can accept their offer. As such, offers should only be open for acceptance by participants 14 days after they receive their offer.

Simplified disclosure materials

Further, your company must provide participants with the following materials at least 14 days before either of the following occurs:

-

The participant exercises their option; or

| Documents | Description |

| Financial information | Financial information includes:

|

| Valued information | Provide a copy of the valuation of the option or shares. Common valuation methods are those approved for tax purposes, which include:

|

| Solvency statement | You must provide a statement that the company is solvent. |

Your company must provide these materials before the participant’s options become exercisable, even if they do not choose to exercise their option. Consequently, consider whether to limit the dates on which options become exercisable under your ESOP by either:

-

Nominating a specific exercise period each year; or

-

Using an ESOP that only allows exercise upon an exit event rather than exercise upon vesting.

If your employee equity plan is a share plan and not an ESOP, you must provide these materials when issuing shares to the participant. In other words, you must provide these materials when you give the offer document.

Other requirements

There are further requirements you must meet if your ESOP includes:

-

A trust arrangement; or

-

If you help your employees acquire securities under your ESOP, such as by providing a loan.

If your ESOP contains these features, you should speak to a qualified lawyer.

Key takeaways

New disclosure exemptions are in force from 1 October 2022, making it less demanding for startup owners to issue an Employee Share Option Plan (ESOP) to eligible workers. If you wish to make an ESOP offer to more than 20 persons within 12 months, you no longer need to comply with certain disclosure obligations. Instead, your ESOP offer and its terms must follow the new employee share scheme rules.

For assistance in making an ESOP offer that complies with the new disclosure exemptions, LegalVision’s experienced startup lawyers can assist as part of their membership. For a low monthly fee, you will have unlimited access to lawyers to answer your questions and draft and review your documents. Call LegalVision today on 1300 544 755 or visit their membership page.

Disclaimer: The above article is for informational purposes only and does not constitute a specific product recommendation, or taxation or financial advice and should not be relied upon as such. While we use reasonable endeavours to keep the information up-to-date, we make no representation that any information is accurate or up-to-date. If you choose to make use of the content in this article, you do so at your own risk. To the extent permitted by law, we do not assume any responsibility or liability arising from or connected with your use or reliance on the content on our site. Please check with your adviser or accountant to obtain the correct advice for your situation.

FURTHER READING

Save time and money by sharing your portfolio with your accountant

It's easy to save time and money at tax time by sharing access to your Sharesight portfolio with your accountant. Keep reading to learn more.

Morningstar analyses Australian investors' top trades of FY26

Morningstar analyses Australian Sharesight users' top trades of FY25/26. Keep reading to see some of the most notable picks from the year.

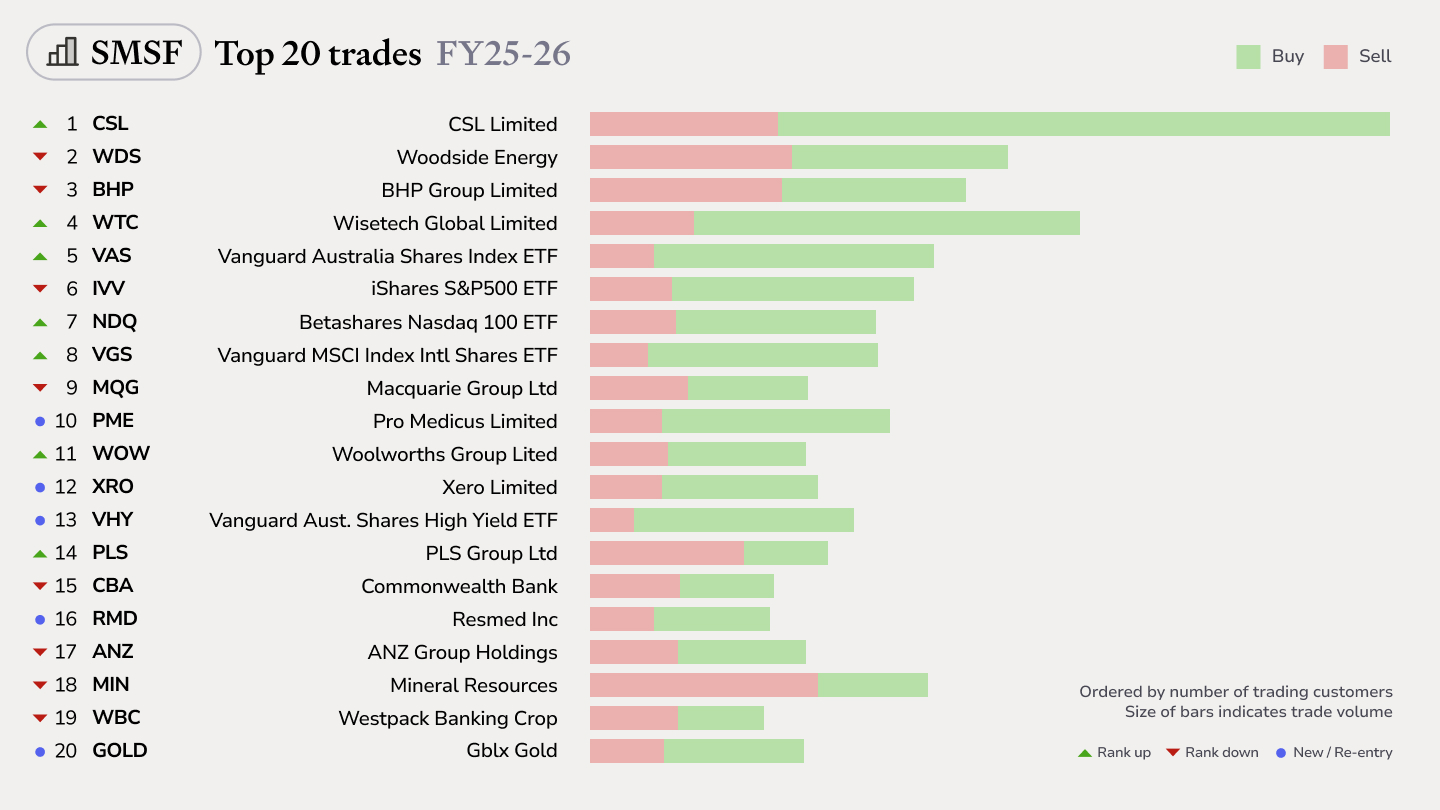

Top SMSF trades by Australian Sharesight users in FY25/26

Welcome to our annual Australian financial year trading snapshot for SMSFs, where we dive into this year’s top trades by Sharesight users.